Happy New Year, everyone! It’s time for me to write another portfolio & savings update for Q4-2023, so I can continue documenting my journey toward one million Euros and get the books up to date. It’s also a good time to look at 2023 numbers, income, expenses, savings, returns, and some thoughts and conclusions for the year.

Table of Contents

Q4-2023 In A Nutshell

This last quarter of the year was super quiet. We needed this after our marriage and a two-week trip to the US. We spent Christmas days at home, and then we travelled to the South of England to spend four days, including New Year’s Eve, with old friends. It was lovely. We visited Brighton for a day, the city where my wife and I met. This city brings so many memories of my first days in the UK. Those times when I could barely speak or understand any English. What an adventure that was! It got me reflecting not only on 2023 but also about all these years to today. 2024 will mark my 10th year since I first landed here. I can clearly remember my first day. I had just landed at Gatwick Airport when I realized I couldn’t understand a damn thing of what people were saying (despite many years of studying English). My sensation of fear increased as I was getting away from my circle of confidence, and it would take years before I would feel 100% confident with myself once again. It took a lot of bloody digging, a lot, but I could not be the person I have become today without taking a spade with both hands. Anyway, maybe I will spend more time writing about my past diggings in my 10th year, but for now, I feel that is enough.

On the new home side of things, we continued to do some DIY work here and there. The next step is refurbishing the bathroom. B&Q (the DIY store in the UK) is offering a 25% discount on bathrooms in January, so we want to complete the design and buy all the components before the end of the month. B&Q also offers installation services, but I’ve decided to look for a local installer after reading about other people’s negative experiences with them. We are happy with the guy who installed our new kitchen, so I am trying to get him to quote for me, but he is always very busy, which is a good sign. It’s hard to find good builders in the UK, so unless you have a recommendation from someone you trust, hiring a good builder is mostly about luck.

At work, I received my promised pay rise. Nonetheless, the workload is below the normal average. The business projection for this year is not optimistic, so unless things start to gear up soon, the risk of losing my job again is high. I am not worried about this at all, as there’s plenty of work available around the area, but it’s more about me wanting to see the small company thrive and grow.

Quick Recap of Q4-2023 Numbers

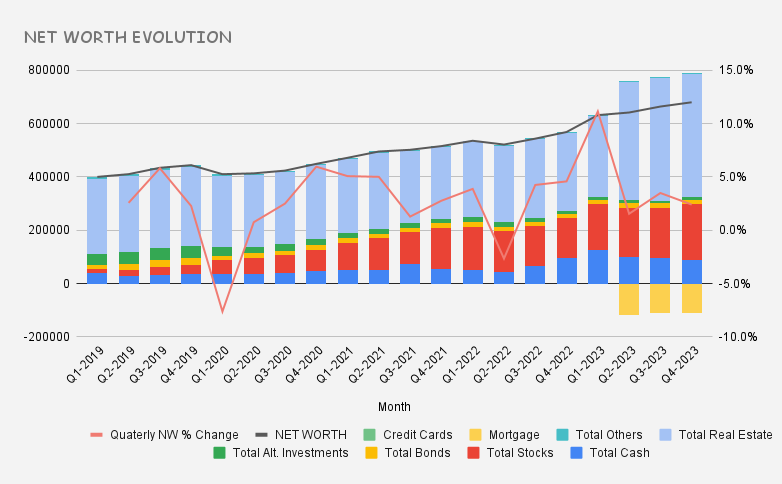

- Net worth: €680,150 (+2.4%) – details HERE

- Portfolio value: €237,110 (+9.33%) – details HERE

- Quarterly Total Growth: €20,246

- Quarterly Savings Rate: 20%

Comments

Stocks have been on steroids this quarter, and so has been the growth of my portfolio. As I am gradually increasing my exposure to stocks, my net worth is also slowly becoming more prone to fluctuate with the rhythms of the stock market.

I only saved 20% of my total income, as the wedding and trip made a deep dent in my finances this quarter.

Quick Recap of 2023 Numbers

Now, let’s compare 2023 numbers against 2022’s.

My net worth at the end of 2022 was €568,574. Compared to where it sits now, it’s an increase of €111,576. This was my best year in terms of net worth growth, a nearly 20% annual increase. This is motivating to see and drives me to keep pursuing my financial goals forward.

Below is a breakdown of my net worth value from 2019 to date. The trend is clear. Bonds have remained mainly flat, stocks have taken more protagonism, my stake in alternative investments has been reduced, my cash reserves ended the year lower, and a mortgage was introduced this year as well.

My investment portfolio was €181,684 a year ago. That compared to today is an increase of €55,426. That’s a 30% annual increase, another awesome result that couldn’t be happier about!

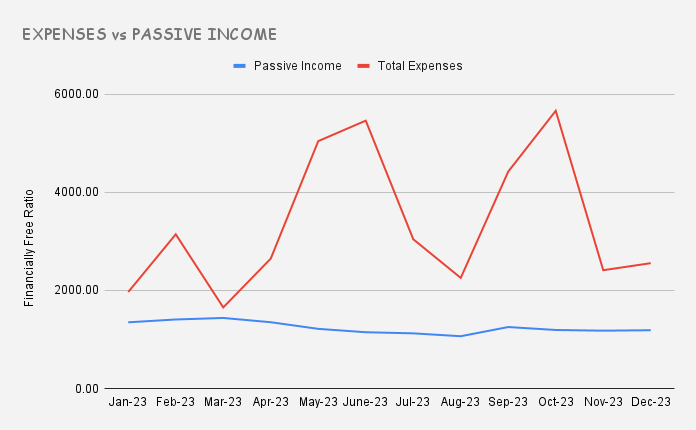

Total taxable passive income for 2023 was €17,157. This also increased in 2022, mainly thanks to higher interest rates and rent increases.

As the chart above shows, I don’t focus my investment contributions on generating passive income, as this has remained flat over the months. The two spikes in my expenses are related to house purchasing plus moving expenses during May and June, and the wedding and honeymoon expenses during September and October.

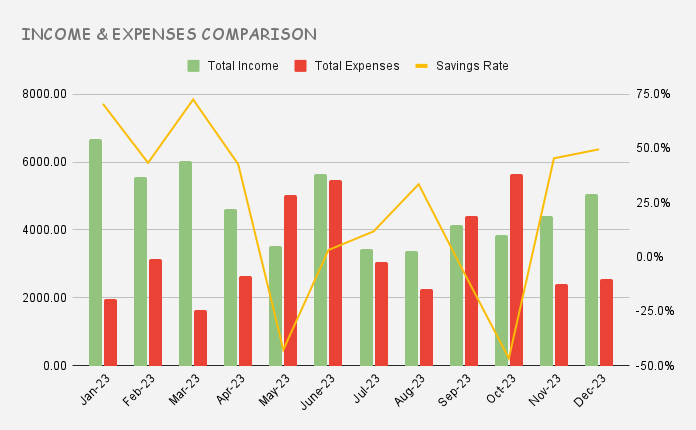

In total, I spent a whopping £40,262 this year. That is a monthly average of £3,355. I don’t even want to exchange that for Euros as it is painful enough to see as it is, haha!

Income and Expenses 2023

This is the final outlook for my income and expenses in 2023:

My savings rate for this year is 28.6%. To be honest, I am glad I managed to save any money, as both buying a house the first time and marrying are not cheap. I don’t expect to hit a savings rate of 50%-60% as before. We have to pay back a three-year 0% interest loan which we used to buy the new kitchen, and we may ask for a new one to pay for the upcoming new bathroom. I don’t expect to surpass the 40% savings rate in 2024.

This is a breakdown of my income for 2023:

I had a strong start to the year generating side hustle money, then I stopped as I needed free time to move out, settle and make house improvements. Now I have some more free time, so I’ve started doing some matched betting again. I won’t be able to generate as much cash as I used to with doing design work, but every little helps. The good thing about match betting is that you choose how much time you want to spend on it and when. When I was doing design work, I had to hit deadlines, which put a lot of stress on me at some points. Though I miss earning that extra money, my mental health is thanking me for not doing it.

Investment Portfolio Breakdown

This is how my investment portfolio breakdown looks for the end of this year:

Please note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these platforms.

** 20 % discounted to estimate future withdrawal tax payments

The annualized returns are only indicative because of simpler calculation reasons. I know that in real terms the returns are a bit higher (for the investments that I contribute, currently, pension, ISAs and Dividend Portfolio). However, they are good enough to compare returns. I am very disappointed with the returns of my S&S ISAs and not so convinced about the returns of my dividend portfolio. My pensions got better returns even after applying a 20% future tax reduction.

This is a breakdown of all my investments in my ISAs taken from my index fund portfolio. I can see that the answer to my ISAs bad returns is Bonds, Emerging Markets and Global Clean Energy ETF. I have decided that I am going to simplify this even more and get rid of Bonds and Emerging Markets at some point in 2024, and just stick to an All-World Tracker.

The iShares Global Clean Energy ETF I want to keep as it is part of my old forgotten but not forgotten 45K Project Fund, which by the way I owe an update in 2024 since it will be the 5 years since I stopped smoking :D. I wonder how big this fund will this be by then, and how much I have left to hit 45K.

About P2P, I am stuck with them and have not been able to withdraw money for a while. Crypto and especially Bitcoin is getting traction again. There’s a Bitcoin halving in April. It could be a good time for me to sell all my Crypto.

Dividend Portfolio

Now as usual I get to look into my dividend portfolio which generated €183.7 of passive income this quarter (€170.87 last quarter).

The total dividend income of this year was €810.35. The previous year was €710.75. As I didn’t contribute cash this year, that’s €99.6 or 14% of annual organic dividend growth, which is pretty positive.

I didn’t have any dividend cut in 2023, however, the Walgreens CEO recently announced a dividend cut by almost half, which is not a great start to the new year. I would like to give the new CEO a 12-month shot as the sales of the company are growing and look positive, although I will want to see some improvement in the next two quarters.

Here’s an overview of my monthly dividend income so far:

The end-year returns for my dividend portfolio are 7.85%, that’s nothing compared to the 22% of the world tracker. This has demotivated me and got me thinking that perhaps I should just stick everything to world funds.

I enjoy investing in dividend stocks, and it is fun, but is it becoming a too expensive fun to have?

Final words

2023 was a fantastic year.

I finally bought a house and settled in nicely, I got married to my other half, got a good raise, enjoyed and learned a lot at work, exercised regularly and felt healthy and happy, met some new friends, travelled to Italy and the US and my net worth and portfolio skyrocketed.

What else could I ask for?