Portfolio & Savings Update #42 Q4 2022 + Full Year – €181,684

Happy new year! It’s time for me to write another portfolio & savings update for Q4 2022, so I continue documenting my journey toward one million Euros and get the books up to date. It’s also a good time to look at 2022 numbers, income, expenses, savings, returns, and some thoughts and conclusions for the year.

Table of Contents

Q4-2022 In A Nutshell

In Q4, I enjoyed a pay rise from my employer, which is always welcome. However, despite the rise, I am still at the same wages as I was two years ago. Day-to-day life is cheaper in the north compared to the south, so you could think that this compensates for my stagnated wages, but when you add up the inflation values of 2022 that compensation is not enough. Looking at 2023, I believe I could find a better-paying job, but I fear this could impact negatively a mortgage application, so I am trying to just keep going and don’t think too much about my loss of purchasing power.

It’s true though that I have a separate source of income from my previous employer, as I still keep doing some work for him as a sole trader/freelancer. Pre-Christmas time was hard for me, as I got pressure from both bosses at the same time just when my father-in-law passed away, which involved flying to the Czech Republic and back one week prior to Christmas. I entered into the slow killer spiral of stress + lack of sleep + tiredness + bad eating habits + grumpiness. It made me realize that I need to slow down as I could notice my health deteriorating quickly, and fixing my health is not something I’d like to use my savings for.

So here goes the first conclusion of 2022: I am going to take it easier in 2023.

On a separate note, this quarter, we also started house hunting (now a bit more seriously). We obtained our mortgage in principle, which is good, but only viewed two properties since then. The first one was cheap, for £145K, but was too old and the floor would swing as you walk on, that was a no way. The second one was lovely but rather pricer for £245K, we put down an offer on that one though, but another buyer offered more, so we lost it. Then we were to view a third one when the seller decided to increase the asking price one day before the viewing, so we cancelled the viewing. We are first-time buyers with no chain. This plus the fact that we are entering into a buyer market period means we’ll take it easy for now. The only thing that is not easy is my patience, as I want a house, NOW!

Ohhmmmm…. Ohhmmmmm….

Quick Recap of Q4-2022 Numbers

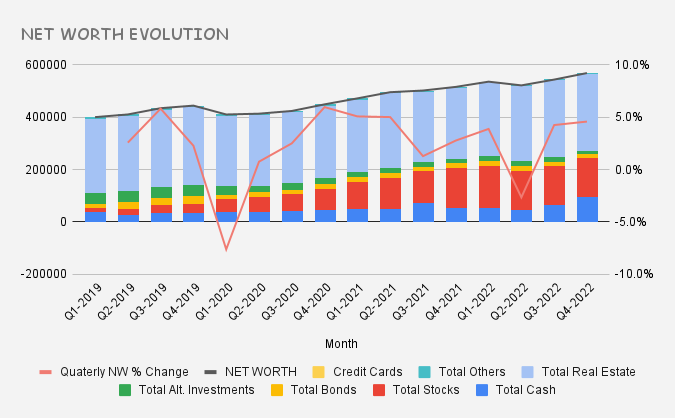

- Net worth: €568,574 (+4.6%) – details HERE

- Portfolio value: €181,684 (+0.44%) – details HERE

- Quarterly growth from investments: €3,514

- Passive income: €4,181 (€3,680 previous quarter) – details HERE

- Savings Rate: 21.7%

Comments

In December, my uncles managed to sell my old grandma’s house. She passed away five years ago, but her house was neither listed on the market nor rented. I was not aware about this house, as I thought it had already been sold, but it came as a surprise that it actually didn’t. In total, I get to receive €30K from selling, which net is going to be around the €28K. So far I’ve received €25K, I should get the remaining in January. This has benefited my net worth value as it is on the greens despite markets being flat for this quarter.

This has all been converted into Pounds, and it’s sitting in a Zopa and Coventry Building Society savings account, paying over 3% in interest rates. In total, I have over £80K in easy access saving accounts, and if doing the maths, they provide me with a forward interest income of roughly £2,500 or £200/month. This is only temporary income, as first rates won’t be that high forever, and second I will eventually use this cash to buy a house. If we were not looking for a house, I would definitely put this in stocks as I think it’s a great time to buy equities which are highly likely to return more than 3% in the longer run.

Passive income increased, mainly as mentioned because rates are higher, and I am stashing cash.

My savings rate was again badly beaten by another €3,153 I had to pay as inheritance taxes. What bothered me was that I didn’t keep that much cash in Euros, and as Pound as fallen considerably, I opted to sell shares on Global Small Cap Index Fund I have held in MyInvestor in Euros. I obviously had to sell for a loss :(. Luckily share price has continued falling, so I am now rebuying some shares cheaper, hopefully I can recover the loss once the market rebounds (maybe in 2023?).

Quick Recap of 2022 Numbers

Now let’s compare 2022 numbers against 2021’s.

My net worth at the end of 2021 was €515,721, now it’s €568,574, that is an increase of €52,853. Most of the increment is in cash earned and saved but not invested, and the cash received from my grandma’s house.

Below is a breakdown of my net worth value to date. The trend is clear. Bonds have remained mainly flat, stocks have taken more protagonism, my stake in alternative investments has been reduced, and my cash reserves have been increased this year.

My investment portfolio was €190,362 a year ago against €181,684 today, that’s a decrease of €8,678. The main causes of this are the lack of performance for both stocks and bonds, the drop in value of the pound against the euro (from 1.20 to 1.13), the decrease of my monthly contributions, and my investment withdrawals from P2P lending that has been converted into cash and transferred to bank savings accounts. Looking at the chart below, I can see how much volatility we’ve had this year. Putting on the side the 2019 event, it was all plain sailing until this year, in which I have barely been able to cross the 200K psychological resistance zone.

Total passive income for 2022 was €15,216. Although I know it’s increased thanks to raised interests and dividend growth, I can’t compare this value against 2021 as I only started counting the rental income from our warehouse in mid 2021. I will be able to compare in a year-to-year basis from next year.

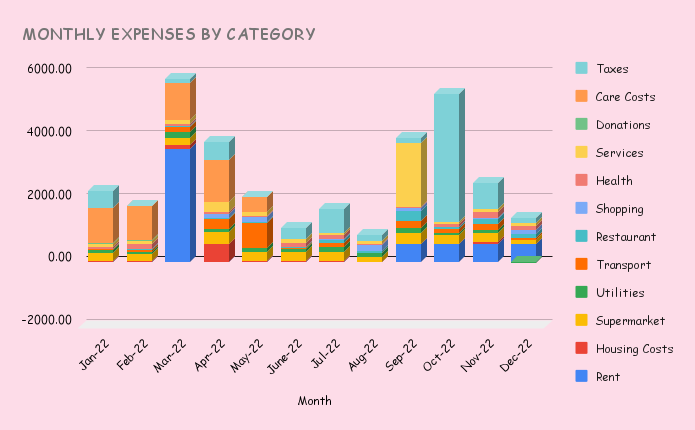

Passive income was steady throughout 2022, although the same can’t be said for my expenses. In March, we moved back to UK and had to pay 6 months of rent in advance plus bought small home appliances, from September to November, notary, inherence and other taxes had to be paid so hence the second spike. What a rollercoaster year it has been, or at least that’s what the chart is telling me.

Income and Expenses 2022

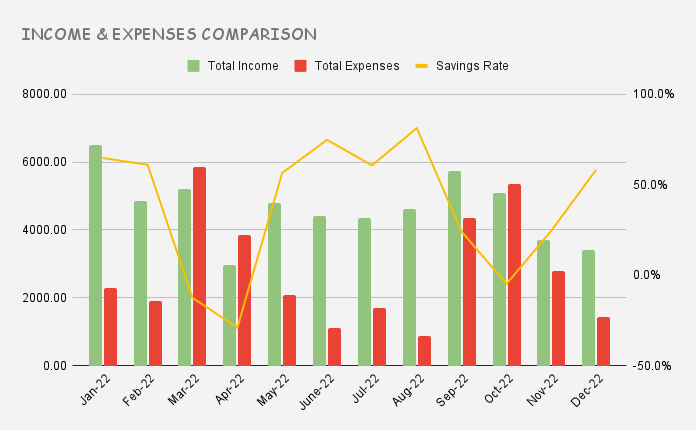

This quarter, savings amounted to £2,656 (3,001 EUR).

This is the final outlook of my income and expenses in 2022:

What about my savings for this year? Well I saved £22,801 in 2022 compared to £32,185 in 2021. Last year, we lived in my hometown flat for 9 months, so I saved on rent. I also spent more this year because of the inheritance cost. Despite being an expensive year, I managed to save a decent amount. 22K is enough to max out my ISA contributions for one tax year.

This is a breakdown of my income for 2022:

Portfolio Performance

Next, we move to analysing my portfolio performance for both this quarter and the full year:

Please note, links containing a star (*) are either affiliate or referral links. P2P lending is a risky business, so you could end up losing all your invested money if you choose to join any of these platforms.

** 20 % discounted to estimate future withdrawal tax payments

In Q4, I fully exited successfully two investment platforms, that was Qardus and Reinvest24. I am happy with the final performance of both, which has been 12% and 12.5%. It was surprising how fast I managed to sell all my shares in Reinvest24. I placed all my shares on the secondary market, thinking that they would stay there for a while, but all shares were sold in two weeks.

Why did I exist these platforms? You may ask. I had planned a long time ago to exit Qardus, as I only had a small investment and felt like needing some tiding up of platforms. In the case of Reinvest24, I exited because I want to have as much cash as possible ready for our next house. The pound is nearly at ATL against the Euro, so it felt a good time to cash out and exchange currency. I also want to exit the remaining platforms, but unfortunately some I am stuck with them (Property Partner, Housers and Crowdestor) and others charge a fee to sell on the secondary market (Estateguru and Crowdestate) so I rather wait. I already managed to cash out some money from Estateguru, but I have still over €1,5K locked in. In terms of passive income from P2P investments, Reinvest24 and Estateguru were the two that provided me with better returns for the year.

In terms of annual returns, crypto is the asset that has lost more blood, followed by index funds equities and bonds. Bonds will likely recover as soon the interest rates change towards a downwards trend, so let’s hang on in there.

Portfolio growth for the year was negative at -€15,989, I think this give a negative return around the like of –8% and -10%. I don’t think I can trust much these values, as the pound was very volatile, and it’s hard and time-consuming to calculate an accurate return. The clear picture though I think is that I’ve still done better than the S&P 500 (-19.5%) which is never a bad thing 🙂

My total portfolio return finished at -18.3%, compared to a -7.3% the previous year, OUCH. Let’s hope for a better 2023?

Dividend Portfolio

Now as usual I get to look into my dividend portfolio which generated €170.8 of passive income this quarter (€181.7 last quarter).

Total dividend income of this year was €710.75. The previous year was €390, so that’s a 45% YOY dividend growth. Part of this growth, though, it’s been via new contributions to my dividend portfolio. I contributed a total of €5,596, which is a 42% increase compared to 2021. Also, the strong dollar increased my dividend payments in euros.

Two companies cut their dividends, that’s AT&T and GlaxoSmithKline after they split part of their business. With AT&T, I am deep in the mud, I am taking a no dividend reinvest and wait and see approach, with GlaxoSmithKline I am betting on a turnaround, a riskier bet for sure, but their wider moat gives me hope.

Here’s an overview of my monthly dividend income so far:

I started my dividend portfolio as an experiment three years ago, and my impressions are positive. It’s a reliable investing strategy and income building machine. Thanks to the dividend income, my dividend portfolio ended positive for the year, while the S&P500 dropped over 19%. Even the 3Y return of my dividend portfolio is higher than the S&P500’s, which sounds unreal, though I don’t think my dividend portfolio can beat the market over the l/t.

My first Growth Stock Buy: Alphabet ($GOOGL)

Recently I got to read a new interesting book: “Scary Smart” by Mo Gawdat.

Mo Gawdat is the former chief business officer of “Google [X]”, now called “X Development LLC”. This is an American semi-secret research and development facility and organization founded by Google in January 2010, which now operates as a subsidiary of Alphabet Inc. Here is their website.

I still got to finish the book, but what I’ve read so far has been enough to open my eyes on the future of AI. The AI revolution is a sure thing to happen, and given that the guys at Google are in the front of the line, It would be madness for me to not buy Google shares at its current prices. I mean, if you just go to their website and check all the projects they are working on at the moment, it is seriously mind-blowing. I can’t wait to see many of these projects taking off, starting with having a reliable self-driving technology. This alone could improve the rail sector in the UK greatly, AI machines won’t go on strike and f*ck up your journeys despite paying through the nose for a ticket! Increased efficiency and reliably for a cheaper price, this is what AI has to offer to humanity.

You see, last year everyone talked about crypto and growth stocks, but if you were a dividend investor then you were a “loser”. This year, no one talks about crypto (positively) or growth stocks, but dividend stocks instead. That shows a simple conclusion, dig in the sector which isn’t popular and choose from there. For me now that is Alphabet, I could be wrong obviously, but while prices stay as they are I am definitely going to keep buying! 🙂

Final words

As a final concluding words, I would say that 2022 has been a rollercoaster year for me. I went through some serious sad moments that I want to put behind, buried in my 2022 memories. I am more optimistic about 2023 than most people are, I sense it will be better than most think.

Despite the market meltdown, I shouldn’t complain as my portfolio performed better than the market and I also received an unexpected cash injection from my old grandma’s house that I didn’t even know we still had. That alone saved my net wort values for 2022.

In 2023, I am going to take it easier, and that starts by not setting new goals. I won’t compare my 2021 goals, which I normally do in a separate blog post. I know I have failed on most of them, for instance one of my financial goals was to reach a portfolio value of €240K, I am at €181K… 🙁

I want to try on working a bit less, getting married by the beach 🙂 (hopefully in May if nothing bad happens, which hasn’t been the case in 2021), buying a home in the UK and settling in nicely, have my first guests and my first barbecue in the garden, and then perhaps start giving a though about how I can generate more income without losing my health on the way.

That’s all for this Q4 2022 and year-end. My next update will be in April.

Share this:

ABOUT ME

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

NET WORTH GOAL