One Million Journey Plan – Year 1 Update

Approximately one year ago I sat down determinedly and wrote my own one million journey plan statement. In this post, I intend to do a yearly review of the process and write an informal report to note reflections and corrections made on the original plan. This is the year 1 update.

This is an empowering exercise. It forces me to read my old words, which were written by my old me. This allows comparing my own thoughts between now and then, and make my own conclusions. That’s the big magic of journaling and self-improving along the journey. But this magic only works if we keep repeating it for the long term.

(This post may sound a bit repetitive for long time readers, as I basically collect all the changes I’ve commented along this year and wrote them down on one place.)

Table of Contents

Year 1 Results And Comments

Earlier in October, I updated my net worth numbers for the third quarter of 2020.

The result was 423,779 €.

According to my original plan that value should be somewhere near 478,556 € (image of the previous plan here), which means I am falling short by -54,744 €. That is a substantial amount. Sadly, I am even worse off I was 12 months ago, as my net worth at year zero was 435K €.

But no worries, I remain positive and I always will!

However, it’s worth to ask: Why did that happen?

Well, it happened for several reasons.

First, I assumed that the value of my properties in Spain decreased due to the Covid-19 crisis. In 2019, I estimated an approximate value (20% discounted) of 295K €, whereas in 2020 I accounted for an 8% reduction of that price, which results in a net worth decrease of roughly -24K €. This could drop even further, as my properties are located in a below-average growing rate. My plan takes a 2.2% annual appreciation for my properties in the future, which is the long term average inflation in the area.

Second, I wrote-off my investments with Envestio and Grupeer. Sad to say, Envestio turned out to be a scam and the situation with Grupeer is still uncertain. That made me lose another -8,087€. Albeit I expect to recover some capital back, this is money that is not making me any more money. This has an impact on the long term compounding of my original plan, even if I end up getting back all my money.

That’s why Warren Buffet’s rule number 1 is “don’t lose money“.

Third, the value of the Pound Sterling against the euro is below 1.25, which is the base rate I used for my calculations. Obviously, this is unpredictable, but I expect a recovery after Brexit waters have calmed down. (hopefully before the next 10 years?)

Fourth, my mum’s care added costs have taken a bite on my finances. This means I no longer can expect to use any generated rental income from our warehouse to max out my ISA as these are all mainly used to cover her expenses.

Fifth and last, I changed my investing strategy, which I explain in more detail in the following section.

Changes On My Investing Strategy

Reducing Alternative Investment Allocation

Earlier in 2019, after losing money with Envestio, I reconsidered my portfolio allocation. On my original plan, I was happy with keeping 10% of my net worth invested in alternative investments such as P2P Lending.

Due to the higher risks of investing in P2P, the FCA advice to retail investors is to not invest more than 10% of your investable assets, which is not the same as net worth.

Investable assets include liquid and near-liquid assets, such as:

- Cash, checking and savings accounts.

- CDs and money market accounts.

- Stocks, bonds and mutual funds.

- Retirement accounts and trusts.

Considering that real estate is an illiquid asset and that it makes up 64% of my total assets means that on my original plan, alternative investments consisted of the 40-50% stake on my investable assets.

Problemo amigo, problemo!! 😉

Adding Dividend Income To My Strategy

Reducing my alternative investment allocation meant that I had to go from 47K € invested, down to 10K €, so adding dividend income to my strategy seemed to make sense.

Putting on the side whether this is the best thing to do or not, dividend investing had always called me and I wanted to learn more about it. This together with the dividend tax-advantages we enjoy UK residents and the fact of being able to invest using Euros, made me decide to dip a toe in dividend waters.

I informally introduced my dividend portfolio in February on this post. The bad timing (pre-lockdowns) has hurt my toe, but overall, I remain positive with the long term average returns and dividend growth. On my revised strategy, I based my calculations on a net annual growth of 5% for my dividend portfolio, a rather conservative approach.

More into Pension And Less into ISAs

In 2019, I was very sceptical with the idea of contributing too much into my UK work pension. The fact of holding a Spanish passport while residing in a country that’s planning to split from the UE didn’t help.

However, after investigating a bit more I learned two concepts that changed my mind:

- If I were to move back to Spain, anything that remains invested in my ISAs will become fully taxable. This is painful for my eyes to read. On the contrary, assets invested in my UK pension won’t be taxable until I withdraw funds at the age of 57-60. That translates into 22-25 years or money compounding without paying any taxes.

- The benefits of the UK work pension are just too good to ignore. Employer contributions and tax rebates from the government are free money that will make me more money and compound more. That is not that painful to read, right? 😉

If you are unsure about how work pensions function in the UK, I’d recommend having a read on the government’s site to learn about it.

Because of these pros, I’ve accounted for a 10% annual return on my spreadsheet. I am currently depositing 20% of my payslip income, which is roughly £440.

The Plan (Revision 2)

All that being said leaves me with a new revised plan, the revision 2 plan.

It is still based on the first and fourth CashFlow Quadrant as explained by Robert Kiyosaki, so the core of the plan remains the same.

My main source of income comes from my employer, that puts me in the E (Employee) quadrant. Saving and investing puts me in the I (Investor) quadrant. My cash flows between these two main quadrants.

Obviously, a lot can happen before I hit the million. Workings as a self-employed (S, second quadrant) design engineer is a possibility, but for the time being, I prefer to focus my strategy based from the first quadrant (E), as this will be likely the outcome.

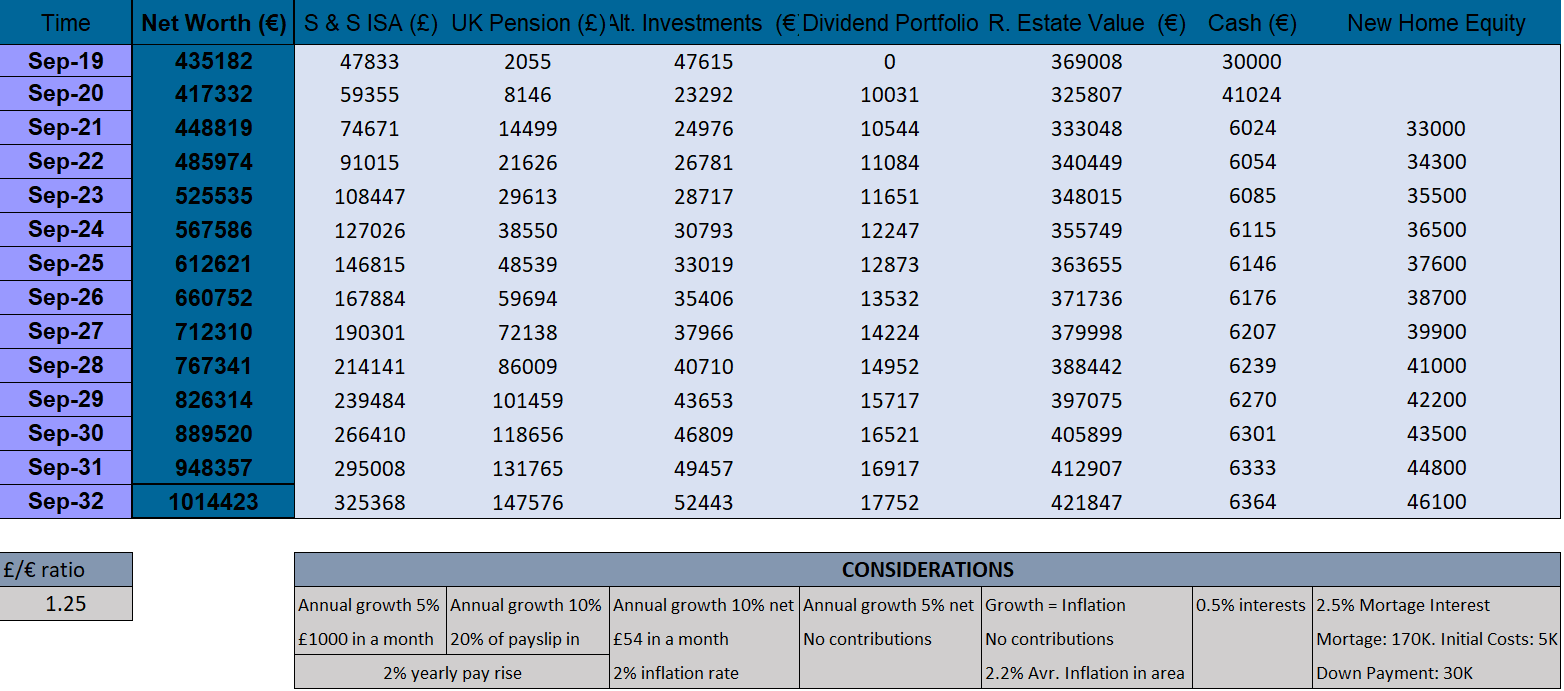

One Million Journey Chart Plan Revision 2

The main goal is reaching a 1.000.000 € Net Worth. This will be more than enough to provide me with financial freedom and long term financial stability.

Stocks & Shares ISA will be my core portfolio. The returns out of this portfolio are tax-free as far as I reside in the UK. I am no longer able to max it out (£20K currently). I expect to contribute £1000 a month into this fund. My investments here will be Index Funds and ETFs, consisting mainly of global funds as I explained here. I will follow a stocks and bonds balanced approach. My current balancing stays at 70/30. I will only rebalance twice per year, in June and December, except during extremely volatile markets, as the one we had in March 2020. My expected annual growth rate for the next 10 years is 5%. This is a fast liquidity account.

Pension will play another important “walk-on part”. I am enrolled in my employer’s pension scheme. Every month I contribute 20% out of my payslip and my employer contributes 3%. I also get tax relief from the government. That approximately sums up £613 a month at the time of writing. All info of how that works is here. I set my investment strategy as adventurous, and what it basically does is to invest in a world index tracker for a 0.5% annual fee. This is more expensive than other world trackers, but it is still worth it if considering my employer contributions. My expected annual growth rate for the next 10 years is 10%. I won’t have access to this account until I am 55 or 57 or 60 or whatever the government decides during the next 20 something years. That’s primarily why my Stocks & Shares ISA is my core portfolio instead of my pension.

Alternative Investments will only constitute 10% of my investable assets. 2020 showed us the real risk of investing in P2P lending assets, therefore I will only contribute my savings on tobacco (£54) or blog revenue to my €45K Project Fund or in other words, ethical investments.

My Dividend Portfolio will also only constitute 10% of my investable assets. I believe that I am not smart enough to outperform market returns. On the contrary, I enjoy reading financial reports and widening my learning about companies that pay a dividend consistently and its sector. Putting a toe in these waters is my personal way of becoming a more well-rounded individual.

Cash provides me with safety and options. Safety in terms of an emergency fund to be utilized in case of unexpected events such as losing my job, health issues or any sudden expense. Options in terms of making a down payment for my future home. I expect to purchase a house at some point during the next two years. This cash will be kept in checking or savings bank accounts.

Net Worth Projection – Millionaire In 12 Years?

I finally come to the point where I need to see when I can possibly expect to become a millionaire.

For all the reasons I stated above, my journey has extended three more years. On the original plan, I was meant to reach the million in ten years, on my revised plan it will be in 12 instead.

I am 35, which means that according to the revision 2 plan, I will become a millionaire at the age of 47. If I round it up, I could possibly fully retire by the age of 50, which isn’t bad. Nowadays, if you are in your 50s you are still young. Life expectancy in Europe for males is around the 80s, so we are talking about 30 years difference.

However, fully retiring has never been my main goal. I am a person who enjoys being active, I enjoy doing stuff and being productive, and I enjoy contributing my part to the world. Life on the couch is not a well-lived life. Travelling around the world sounds exciting, but I don’t think it would be a long term fulfilment experience for me.

Life is about meaning and I can only accomplish that by doing.

As an ending shot, this is how the revised plan for year 1 look like:

Comments, suggestions or questions welcome.

Share this:

11 Comments

Comments are closed.

ABOUT ME

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

NET WORTH GOAL

Thanks T for another detailed update. Does it make sense to keep playing around with the value of the rental object that you have? Do you think it makes more sense to keep it on your accounts at “Book Value”, the value that you paid for it. Until you sell it, you dont know what its real value would be?? adding and chopping values to this asset doesnt make any sense to me, especially if you dont intend to sell it.

Should you increase your 1m target +2,2%per year to keep up with inflation?

All the best.

Hi Steve, thanks for your comment.

Yes and no. I prefer to focus my attention on tracking my portfolio instead of my net worth. That’s why on my monthly updates I don’t count real estate in. But, I like to keep an eye on my net worth on a quarterly basis basically for allocation percentages purposes. The value my family paid for (now) my properties is very low. For instance, the flat cost 1 million pesetas at that time, which is the equivalent of 6,000 Euros approximately. Taking those values wouldn’t be realistic. I apply a 20% discount on the value of my properties to account for selling costs or discounts. Also, we may decide to sell the flat soon, so I want to be informed about price fluctuations in the area.

My current annual expenses are near £12K, Roughly I would only need 300K to be “retire”. The million should be enough to cover future increases in living costs due to inflation (unless we enter into a hyperinflation environment, which I hope we won’t)

All the best, be safe.

Hey Tony- nice post and always good to see somebody that continually revises their goals etc- it’s how we (eventually) manage to get there! My question for you- why are you putting 20% into your employer pension? Surely you only need 5% odd to get the match? If that’s the case, then open a SIPP with the other 15%, and select exactly what fund(s) you want, with (most importantly!) lower fees 😀

Yes! Honestly, I forgot about this! I considered this option after Vanguard introduced their SIPP. I think it only costs 0.15% annually? But then I would need to pay 0.22% to invest in the all-world ETF.

I need to dig more into this, appreciate your input 😀

If extra contributions are made under salary sacrifice then you also save employee NI, and some employers throw in some or all of their employer NI – so worth checking if you have this boost before changing strategy. You could always ask if your scheme allows periodic transfers into a SIPP if you want to optimize for charges…

Cheers

Thank you, that’s a good point. I make contributions under salary sacrifice, do I’ll check these points with my employer. Much appreciated. Cheers

I love your positivity, Tony.

Although your revised plan will take you longer, a millionaire at 47 will still be an incredible feat to achieve.

Funny that you mention that travelling will not fulfill you long term and I feel the same way. I want to do some more travelling but also like spending time at home – travelling endlessly just seems too tiring and stressful!

Regarding the 0.22% all-world ETF fee – this fee is reflected and adjusted within the price/net asset value of the ETF on a daily basis so it’s not the same as the platform fee, which you would see deducted on your statement/account.

I too was going to ask about why you paid 20% into your employer’s pension but salary sacrifice means it makes sense.

Thanks weenie, being negative does not help to get things better, so I am always trying to remain positive although it’s challenging sometimes.

Thanks for your input weenie, I didn’t know that ETFs fees were charged on a daily basis. Good to know 🙂

[…] Tony from OneMillionJourney with a comprehensive review of his plan to become a millionaire by the time he turns 47 […]

[…] One Million Journey Plan – Year 1 Update […]

[…] One Million Journey Plan – Year 1 Update […]