The People’s Pension Vs Nest: Which One Is Better?

I’ve been gathering some information about my two current workplace pension providers; The People’s Pension and Nest, and concluded that considering my financial situation, Nest is a better place to keep my retirement funds for the short-medium term.

In the nine years that I’ve lived in the UK, I’ve worked for mainly three employers, and each used a different pension provider. As you would imagine, I like keeping my finances tidy and simple (if possible), and as such I am prone to keep the minimal workplace pensions open. Previously, after landing my second job in the UK, I transferred my first workplace pension to The People’s Pension, and now that I’ve landed the third one, it was time to decide whether I would transfer all funds to my current employer pension or keep both open.

To make this decision, I considered three points:

- Charges

- Funds Performance

- Protection

Table of Contents

Charges

People’s Pension:

- An annual charge of £4.50 deducted during the scheme year.

- Annual Management Charge (AMC): 0.5% of your pot value, with rebates:

- 0.1% rebate for pots £3,000-£10,000

- 0.2% rebate for pots £10,000-£25,000

- 0.3% rebate for pots over £25,000

- Contribution Charge: None

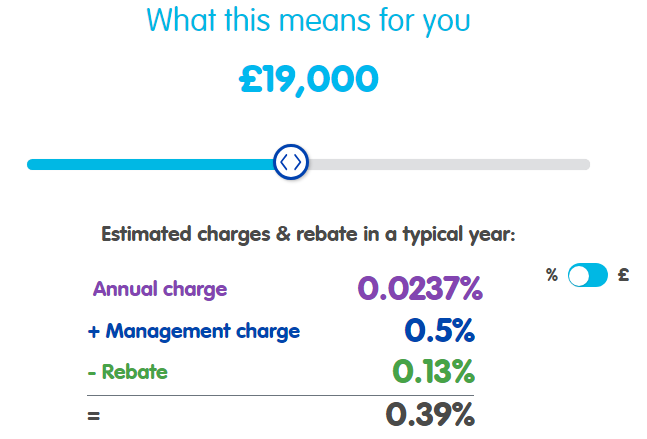

The People Pension’s charges are displayed on their website here, together with an estimated charges calculator that becomes handy to find out what are the final charges concerning the pot size. My current pot size is £19K, which is rather small. According to the calculator, my annual charge in The People’s Pension after applying the rebates is 0.39%.

NEST:

- Contribution Charge: 1.8% of each contribution

- AMC: 0.3% of your pot value

Key Differences:

- Starting point: NEST has a higher initial cost due to the contribution charge, while People’s Pension only charges the AMC.

- Scalability: People’s Pension becomes cheaper as your pot grows due to the rebate system, while NEST has a consistent fee regardless of pot size.

- Transparency: NEST’s fee structure is simpler and easier to understand, while People’s Pension’s rebates can seem more complex.

Which is cheaper?

In my financial situation, given that my pension pot is small, it turns out to be cheaper to invest with Nest, as even after applying The People’s Pension rebates, the annual charges are higher than Nest’s 0.3%. It’s only on pots over the £60K that The People’s Pensions starts to become cheaper. This is more than 3 times the size of my current pot. I won’t be getting close anytime soon.

Putting it down simply:

If the pension pot is below £60K, it is cheaper to invest with Nest, but if it’s higher, then The People’s Pension becomes the cheaper option.

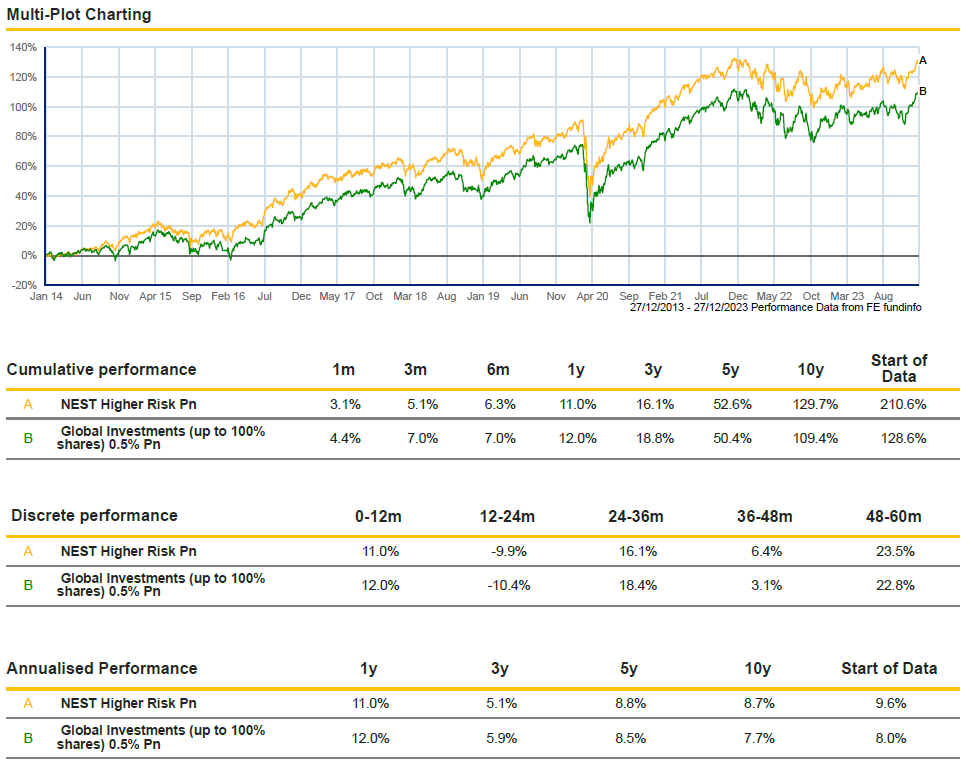

Comparing Performance Of High-Risk 100% Stock Funds: People’s Pension vs. NEST

Both People’s Pension and NEST offer 100% stock funds for high-risk investors, but their performance and characteristics differ.

Here’s a breakdown:

People’s Pension:

- Global Investments (up to 100% shares) Fund:

- Performance: 10-year cumulative return: 109.4%, 10-year annualized return: 7.7%

- Investment strategy: Global equity focus, ESG screened, diversified across regions and sectors

NEST:

- Higher Risk Fund:

- Performance: 10-year cumulative return: 129.7%, 10-year annualized return: 8.7%

- Investment strategy: Global equity focus, ESG screened, with a focus on smaller and mid-cap companies

Here’s a comparison chart showing the performance of the two overtime:

Data taken from Trustnet (https://www2.trustnet.com/Tools/Charting.aspx)

Key Differences:

- Performance: NEST Higher Risk Fund has better 10-year returns and annualized returns.

- Investment strategy: NEST’s fund has a greater focus on smaller and mid-cap companies, which can be more volatile but also offer higher potential returns.

So, on the performance side of things, Nest also gets to win.

Protection

Both are regulated by the Pensions Regulator Guarantee Scheme (PRGS) and the FCA and theoretically, we should be entitled to get back 90% of whatever we have saved in our pension. I take this with a pinch of salt, though, as I don’t think this has ever been back-tested in real life.

However, Nest looks a bit safer than its rival. This online pension scheme was set up by the government to make auto-enrolment as simple as possible. It is the only one I am aware of to be government-backed, which adds that extra layer of safety that The People’s Pension just don’t have.

Conclusion

Nest won all the three points I studied, so it’s crystal clear what the best option is for me. It’s not until I reach a pot size of £60K that I will reconsider my position, but for that, it’s still going to take a few years.

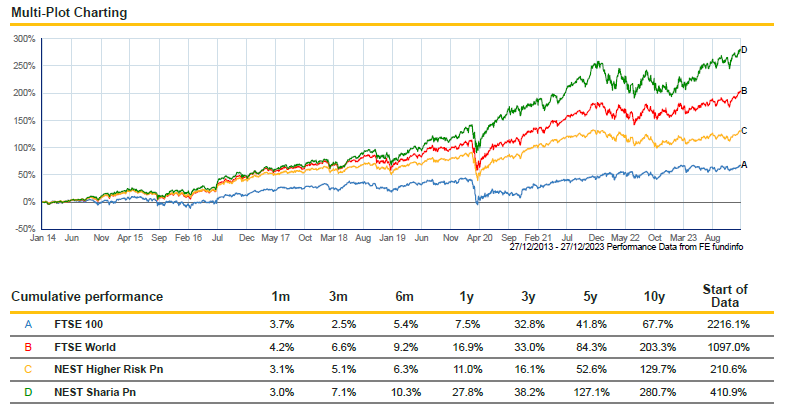

In addition, while doing the performance comparison research, I discovered a Nest fund that has beaten the Higher Risk Fund consistently over the years, and not by just a small margin! The name of this fund is the NEST Sharia Fund. Nonetheless, here’s another comparison chart for the records:

The NEST Sharia fund invests in socially responsible global companies. Some of the top ten shareholdings are Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, and Visa. These have higher percentages than in the Higher Risk Fund, hence why the mind-blowing performance. If interested, you will find all the details of this fund and the other NEST funds on the factsheet.

So, to wrap up, the NEST Sharia Fund may be riskier and more volatile, but given that I still have close to 20 years ahead before I can access my pension, It’s a no-brainer to invest 100% in it.

I am happy to have found out about this fund, it’s one of those things that I would have never come across without keeping this blog alive.

Share this:

1 Comment

Comments are closed.

ABOUT ME

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

NET WORTH GOAL

The People’s Pension also has a Sharia fund that you can invest 100% (or any smaller allocation of course) of your pension pot into but I am unsure how it has performed in direct comparison to the NEST Sharia fund – may be worth exploring them against each other when your pot does approach that 60k mark… unless changes in the charges/fees means it’s best looking at something else by then!