Passive Income – Breakdown

Generating passive income can be stimulating. Sit down, relax and let the money kick in your pockets. What’s not to like, right? In this blog post, I want to do the exercise of grouping the assets of my net worth that generate passive income today or can potentially generate it in the future. This will give me a clearer representation of my passive income streams, and what percentage of my expenses currently cover.

Table of Contents

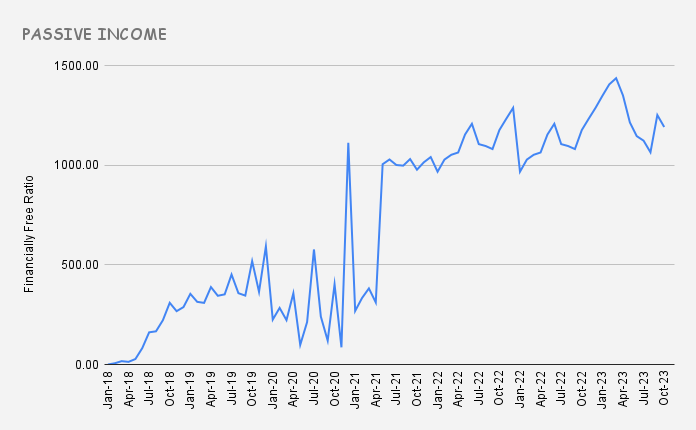

Passive Income Rollercoaster

I’ve documented the trajectory of my net worth and investment portfolio in this blog for a few years. Despite having a turbulent beginning, the valuation of both my net worth and investment portfolio has thankfully increased consistently. However, the same can’t be said about my passive income. It’s been a total roller coaster.

During the first two years of documenting, and up to 2020 I was heavily invested in P2P (approx €50K). At that point, P2P alone was providing me with +600 Euros per month, until we all know what happened — the P2P bubble burst after covid. This asset class turned out to be riskier than I had considered it to be, so my immediate reaction was that I needed to reduce my stake, and so, I did. To date, I am still on the duty of withdrawing whatever funds I can from most of my remaining P2P platforms.

P2P left a void that had to be refilled with something else, less risky. This something else is another personal investing experimentation called dividend investing. I began to reinvest P2P cash leftovers into purchasing dividend stocks. The total return since then is 25%, and I’ve just recently crossed the €2,000 in total dividend payments. I am happy with the “low but steady” results of this experiment, so far.

After the P2P to dividend switch, my passive income dropped substantially at that point as I went from yields of 12%-20% down to 3%-5% That’s one of the reasons why my passive income trajectory looks like a roller coaster.

The second main reason for this sudden drop in income related to a change in my investing strategy during that same year, 2020:

In addition to investing heavily in P2P at the earlier stage of the journey, I also invested in ETFs and bonds that distributed either a dividend or interest payment. I changed that in 2020 to ETFs or funds accumulators, that instead of distributing cash to investors, reinvest cash directly in the same pool, making it this way more cost-efficient for us, retail investors.

All these strategic changes from 2020 onwards drained the passive income stream of my investment portfolio, which is what I report on my monthly/quarterly updates. The investment portfolio doesn’t include other income-generating assets such as real estate or cash.

Passive Income Breakdown

These are all my passive income-generating assets:

- Cash

- Bonds

- Real Estate

- Equities (ETFs, funds, dividend stocks)

In addition to this, in the UK is also popular investing in investment trusts.

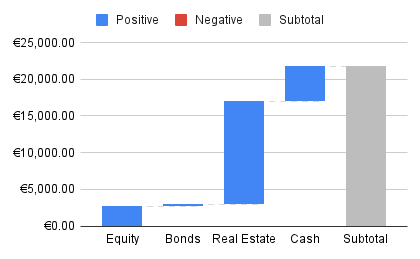

This a detailed breakdown to date:

This breakdown shows the dividend or interest generated by any asset I own now. I include the cash generated by the accumulator funds and ETFs. While I don’t get them distributed to my accounts, I could decide to switch to distributing ETFs and cash in at any time if I want to. This is something I will consider doing at a later stage when I am retired or close to retirement. So having a preview of how much passive income these accumulator funds could provide, can be helpful for me to plan ahead.

This is an overview of my passive income inflow categories by asset class:

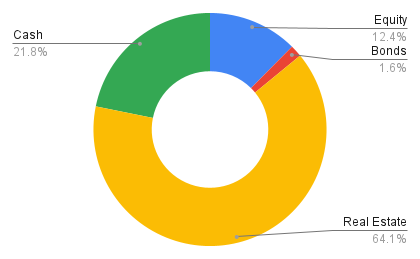

And this is how much in % each asset class contributes to my passive income:

Clearly, the rental warehouse is my biggest contributor to passive income, followed by interest earned on cash.

How Much Passive Income Do I Need To Cover My Expenses?

My expenses over the last few years have varied greatly:

- 2020: £10,498

- 2021: £26,048

- 2022: £33,562

- 2023 (so far): £35,295

Every year was different to the other. In 2020, we spent a lot of time on lockdown. In 2021, I lived in Spain and Portugal and I also spent a lot on my mum’s care needs, in 2022 we moved to Liverpool and spent on inheritance taxes and legal arrangements, and in 2023 we purchased a house, which also adds to the costs.

Despite tracking my expenses for 4 years, I can’t set any of these values in stone, as my situation today is different to any of these previous years. So, what I am going to do is to take these 4 values and calculate the average. The result, which is £26,350, is my expected annual expenses. I think that is more than what I will actually spend, but as the proverb says; better safe than sorry!

Before I do the calculation, I need to convert this to Euros. The result is €30,324 at current exchange rates.

If I now take my projected annual passive income (€21,779) and divide it by this value (€30,324), it tells me that my projected annual passive income covers 72% of my yearly expenses.

That looks optimistic, but given that 22% of my passive income depends on interest rates, it’s likely that it will cover less as rates decrease next year.

Conclusions

A conclusion I take from this exercise is that my passive income is highly dependent on one sole asset. If something goes south with this particular asset, my passive income automatically decreases by 64%.

Even if my projected annual passive income would exceed greatly my annual expenses, I don’t think I would feel comfortable retiring based on this basis. The big picture would change if I had a property portfolio of 10 investments producing this income, as I would know that even if I lose one or two properties I still got another 8 generating cash, but basing your retirement on a sole asset is too risky for me to take.

While I still think it’s worth doing this passive income exercise from time to time, my main focus and retirement pillar is to rely on equity growth and keep on accumulating as described in my plan.

Share this:

3 Comments

Comments are closed.

ABOUT ME

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

NET WORTH GOAL

You should definitely get yourself some more warehouses, Tony! 😛

What is your plan for the coming years then? Do you have a fixed mortgage rate on your new home?

Will you be buying more real estate? 🙂

Hahaha, I see why you are saying that, but I don’t think I want to load the real estate side. I have studied the possibility of investing in BTL in the UK, but the risk-reward balance doesn’t convince me. I was meant to write a blog post about that, so I set that idea in stone but haven’t come around to that yet.

I have not looked into investing in commercial real state, maybe that’s something to dig in a bit.

Our home mortgage rate is variable, we are currently paying 5.69%, but I expect this to come down next year, unless we get into another black swan situation! I renew in 2025 I may consider leveraging if rates are convincing at that time as our house improvements should revaluate the house value 😀

Well look at you being all adult-like and speculating in leveraging your home equity 😛

We are currently at 4% on our flex rate mortgage, but the interest arrow is also pointing down over here in DK, so if it goes back below 3% next year I’ll also consider going back to interest-only, and invest the difference instead.