Grupeer Review – ROI After 15 Months (+20%)

In this Grupeer Review, I share with you my personal opinion and how I have achieved an ROI of 20% after 15 months of investing with Grupeer.

Jump to:

Table of Contents

Introducing Grupeer

Related Content: Mintos Review

Grupeer workforce focuses its attention primarily on business loans and real estate development projects. However, as they are broadening the number of loan originators they work with, it is not uncommon to find other types of loans more often, including mortgage loans, car loans, and personal loans. Loan terms can vary from 3 to 36 months, depending on their current loan originators offers.

Knowing the background of the CEOs and founders of Peer-to-Peer lending platforms is important to me, as I want to make sure I handle my money to the appropriate people. It also gives me some peace of mind – which is sometimes a bit challenging after losing 45K EUR.

Related content: How I Fired 45K EUR Up

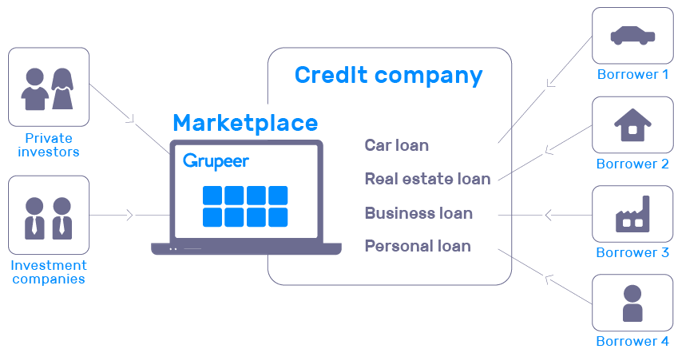

How does Grupeer work?

Grupeer works as a connector between investors and loaners offering a common marketplace through a simple but efficient online financial IT platform.

The image down below summarizes Grupeer’s business model:

Related Content: Investing For Beginners – How To Get Started

Returns to investors and statistics

The average rate of return the investor can expect with Grupeer is 13.5%, at the time of writing. This percentatge stands over the Peer-to-Peer (P2P) European market average of 10%-12% offered by similar platforms like Mintos (12%).

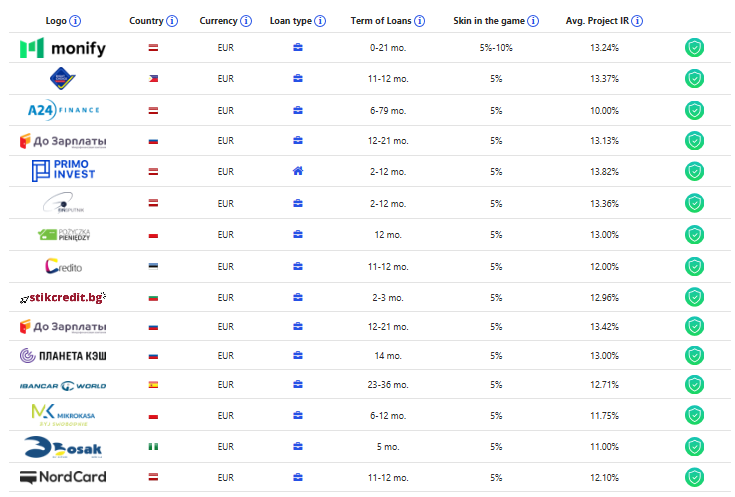

Grupeer loan originators

Loan originators are an important aspect to consider when investing via Peer-to-Peer lending platforms.

You are only able to see basic data, such as the registration number, the number of employees, skin in the game, loans defaulted, loans funded and others. The financial

So far, none of the loans listed on Grupper platform has defaulted, achieving an impressive 0% default ratio since the launching date – two and a half years ago.

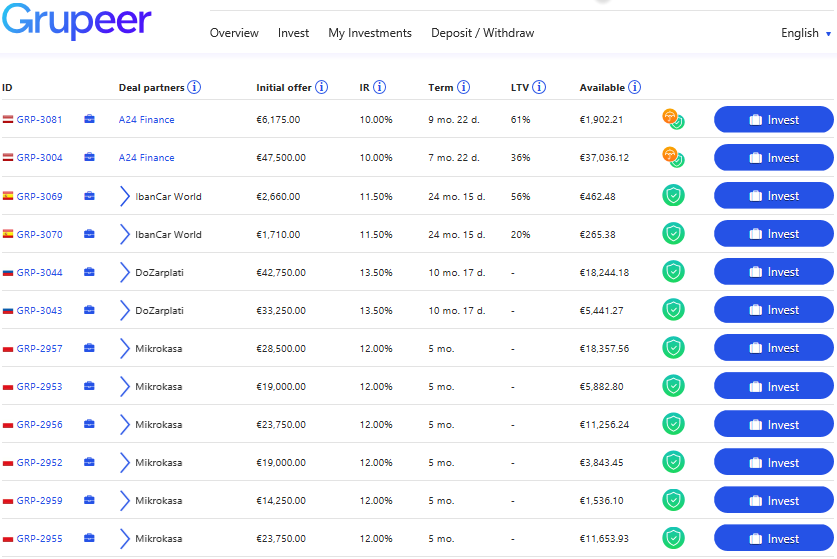

Buyback guarantees and collateral

All loans listed on Grupeer are protected by the Buyback guarantee and others have collateral.

In case a borrower defaults on the interest payments over a period over 60 days, the loan originator must buy back the loan and return the principal and accrued interests to investors.

As an additional guarantee, some loans are secured by collateral, like corporate assets or shares, real estate objects, cars, and personal guarantees among others. The LTV rates can vary significantly, from 20% to 70%

Here are a few examples:

The green symbol at the right means that the loan is covered by the Buyback guarantee. The orange symbol (umbrella) means that the loan is also secured by collateral (first two loans).

From my point of view, a 10% ROI on a double secured investment is a good deal if you want to be cautious, although there may be other risk factors that need to be considered, like the event of Grupeer’s or a loan originator’s bankruptcy.

Finally on this section, I’d like to add up that the loan book/investor ratio is adequate, as there seems to be loan availability most of the times, decreasing the changes of lowering your returns by a cash drag issue.

Grupper financial health

October 2019 update: Grupeer released the financial statements as promised. See my comments and further info on my October 2019 Monthly Update

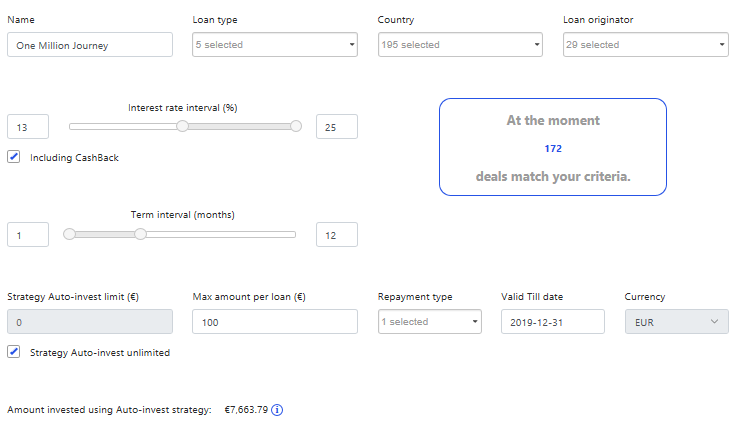

Grupeer auto invest

Grupeer offers to investors an

The auto invest feature in Grupeer has been improved several times. It allows you to set up loan types, countries, loan originators, interests, terms, limits, repayment types, among others.

Once you have chosen your desired criteria, the auto invest tool will let you know about the current loan availability on the platform, so you can readjust accordingly.

As I plan to invest in Grupeer over the long-term, I keep a simple auto-invest strategy, which I check out once a week to ensure it works well under the current marketplace conditions and has no cash drag that could affect my returns negatively.

Secondary market

A secondary market is not available at the moment.

On the meantime, the investor must be aware that their investments will be locked in until the loans have reached the maturity date, so make sure you won’t need the money before investing with Grupeer.

Grupeer Fees

We better enjoy it while it lasts, as it could change in the future.

For instance, take the example of Property Partner, changing its fees structure overnight.

Related content: Property Partner Stabs Their Small Investors

Regulation

The platform is not regulated by any major financial regulator like the FCA. However, it is subject to a set of laws and regulations under the jurisdiction of the Republic of Latvia and directives of the European Union.

Grupeer Taxes

Who can invest with Grupeer?

Personal investors and legal entities can both invest via Grupeer.

Individuals must be at least 18 years old, be residents of the European Economic Area or Switzerland and hold a licensed European bank account.

Grupeer future outlook

Like in every business, there is a past, a present, and a future. As we’ve seen so far, things have been going well in Grupper, but what about its future? What are the managment plans in order to keep a long term sustainable platform?

Let’s dig into to.

Grupeer Stability Fund

The most promising part is perhaps what the company calls the Grupeer Stability Fund. It seems it will give the option to buy a square meter in a real estate property, becoming a

The project is still on early days, and the available information is scarce, but it could be an interesting project to follow for those who want to invest in buy to let in the Baltics in the near future, similar as Reinvest24, Housers (covering Spain, Italy and Portugal) or Property Partner (UK) do, among others

Related Content: Property Partner Review & Housers Review

Move to Ireland

Grupeer new platform aggregator

The platform is studying the possibility of programming a platform aggregator, where investors will be able to diversify across different platforms via Grupeer, however, this project isn’t the main focus for the time being.

Grupeer referral program

Grupper offers to all investors a referral program, giving you the option of earning an extra income if you want.

As per its website:

Referral income is paid for all investments made within 6 months by users, registered by following the referral link.

Referral income depends on the term for which the investment is made:

- investments for a period up to 3 months: referral income 0.50% of the investment;

- investments for a period from 3 up to 6 months: referral income 0.70% of the investment;

- investments for a period from 6 up to 9 months: referral income 1.00% of the investment;

- investments for a period from 9 up to 12 months: referral income 1.00% of the investment;

- investments for a period of more than 12 months: referral income 1.25% of the investment.

Grupeer sign up raffle: 20 EUR

The winners will be announced in my September monthly update. GOOD LUCK! 🙂

I’ll obviously get a commission if you sign up via my link. My profits will ALL be donated to a charity by the end of 2019, thank you. Read my disclaimer at the end of this post.

Further info

- Minimum investment amount 10€.

- Interest rates on loans: From 10% to 15%.

- Payment methods: Bank transfer only.

- Limit payments: EUR 50K a month.

- The base currency is EUROS.

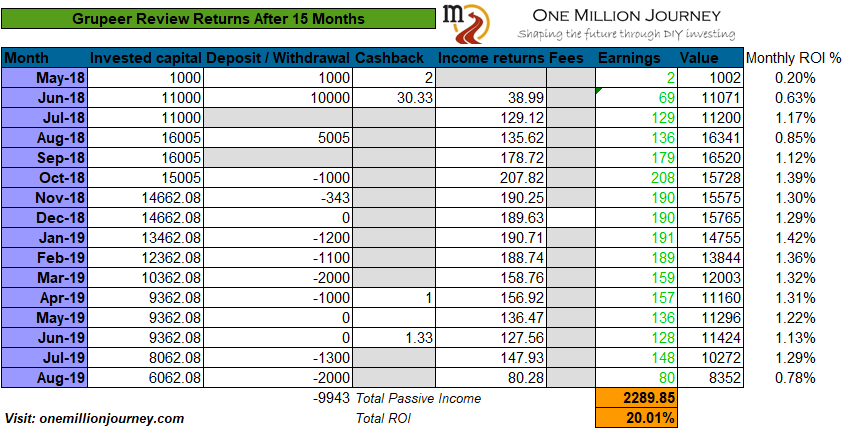

My returns after 15 months of investing

Highlights

- Portfolio value: 8,352 €

- Transactions (Deposits – Withdrawals): 16,005 – 9,943 = 6,062 €

- GROSS earnings after 15 months (Portfolio Value-Transactions): 2290 € (ROI=20%)

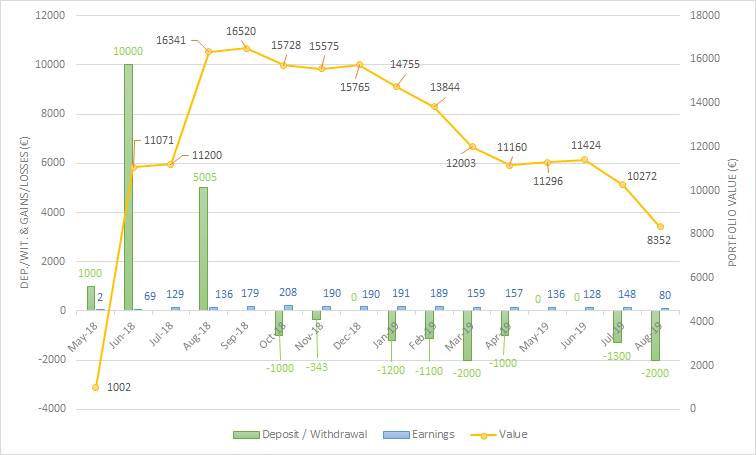

Portfolio performance

As the chart shows, I opened an account and started investing with Grupeer in May 2018. At that time there was numerous cashback offers available. Also, the well-known Promeneda project was funding with a 15% interest rate. I was hungry for passive income, so I deposited over 16K in a three months period.

Since then, Grupeer has supplied me with a realiable source of monhtly passive income. I haven’t experienced any delays, defaults or unexpected events so far – fingers crossed.

As I have been learning over this time, diversification is key in terms of reducing your portfolio risk. So, albeit being happy with the platform, in October I began my diversification process as some loans reached maturity. This is what I have been doing since then, and the reason why the yellow chart line has a downward trend. Up to date, I’ve withdrawn 8 times and got my money into my bank account after 2 or 3 days, as promised.

See all transactions and monthly returns detailed as per follows:

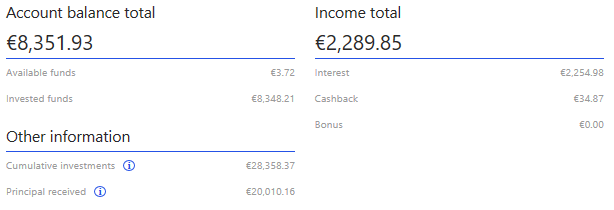

This is an screenshot of my dashboard overview:

Grupeer VS S&P500

During the same period of time, the S&P500 price has increased by 4.6% against the 20% Grupeer returns. This is not counting the S&P500 distributed dividends, which it is currently 1.8% – still, the difference is big.

Conclusions

Positives

- High returns 10-15%.

- No fees or taxes withhold boosting returns.

- Simple and easy to navigate website.

- The future outlook looks promising.

- Adequate loan book per investor ratio. No cash drag.

- The minimum investment is only 10 EUR, again this is good to avoid large amounts of cash drag and boost returns.

Negatives

- No secondary market.

- It is not profitable yet.

- Not regulated by any major financial regulatory body like the FCA.

- Not all documentation is transparently displayed yet (Grupeer’s and loan originators’ financial statements)

Final Words

Grupeer stands out to be one of my favourite peer-to-peer lending platforms, which has delivered a solid and reliable source of passive income so far, making it an interesting alternative to Mintos.

However, past performance is not an indicator of the future and things can turn sideways at any time. The average returns in Grupeer may be higher than other P2P platforms, but the risk is also higher from my point of view, as the company isn’t profitable yet. This is something that should be taken into consideration.

Personally, I plan to continue investing via this platform over the long term, as long as they keep up with their reliability.

Before you go, have a look at my latest monthly review, where you’ll be able to see how my investments on the platform are progressing since this post was written.

Disclaimers

I’m not paid or employed by Grupeer. I have invested and continue to invest my own money through this platform. The sign-up links on this post are affiliate links. When you sign up for an account through my website, I may receive a referral fee, and sometimes you will get a commission too.

I plan to donate 100% or any earning made from referrals throughout 2019. For more information visit my about page or blog post ‘The reasons behind One Million”

** This Grupeer review is for information purposes only and should not be regarded as investment advice. Opinions expressed in this Grupeer review are current opinions based on my own personal experiences. Investing contains risks, so never invest more than you can afford to lose. **

Share this:

2 Comments

Comments are closed.

ABOUT ME

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

{kind=link}

{kind=link}

{kind=link}

NET WORTH GOAL

Solid post! I hadn’t heard of Grupeer before. It is nice that Grupeer allows you to invest in a variety of different use cases.

I’ve been investing in personal loans with LendingClub for a few years now. I am interested in diversifying to another platform at some point.

Thanks Nate for your compliment.

Grupeer is a much younger platform than LendingClub but it has provided on time, solid and high returns to its investors so far. I have big expectations for this platform.