Why Am I Selling My Flat? – Analysis And Numbers

I am selling my flat. The quick answer is that real estate investments are not easy to manage.

Sure, you’ll find content creators like YouTubers, bloggers, or people on Twitter saying the opposite to attract your attention, but from my own experience, real estate is not that simple as it is sold on the web.

Whether you plan on buying a home or investing in physical real estate, there are several factors that need to be considered carefully before pulling the trigger.

A few months ago, I took the decision to sell two of my family properties in Spain, a garage which I’ve already sold and a flat that I plan to sell shortly.

When I told this to my old friends, they all had the same reaction: “you are making a mistake, it is better to rent it, so you get rental income coming in every month!”.

The level of financial literacy of my old friends is lower than mine, but even so, they made me doubt whether I was truly making the right decision or I should perhaps consider renting.

At that stage, I decided to do some research and run some numbers, just to validate my decision and stabilize my peace of mind back to normal levels.

So, in this blog post, you’ll read the analysis and process I followed in single steps. I’ll then go through the final numbers that confirm that selling is the right financial decision for me.

Bear in mind that I am not a real estate professional analyst or anything similar, I’ve just Googled and applied common sense to my calculations, that’s all. Also be aware that this relates to Spain, as it’s where the property is located. Some numbers could vary depending on the country, for instance, in the UK you don’t pay taxes for selling whereas in Spain you (unfortunately) must do.

Table of Contents

1. Determining a Sale Price

A home’s sale price is that on which both, the seller, and the buyer of a home agree.

Obviously, I won’t know the final price until I have found a buyer who is willing to pay for the agreed amount, but I need to use a sale price for my calculation, preferably as close as possible to the final sale price.

How do I find it?

By simply searching sold property prices of similar flats around the neighbourhood. In my case, I used the following methods:

1- By word of mouth with neighbours.

2- By checking local property market statistics.

3- By checking online listings.

By talking to neighbours, I found out that a flat near mine had been sold for €60K recently. However, mine is newer, and the kitchen is completely redesigned. These two characteristics mean that the selling price of my flat should be higher than €60K. That was useful information to give me an idea of what I could at least aim for.

I also checked online listings, but I couldn’t find anything comparable. The latest listed flat “as sold” was one year ago. I can’t use this as a reference, as property prices swung largely during the pre and after covid times.

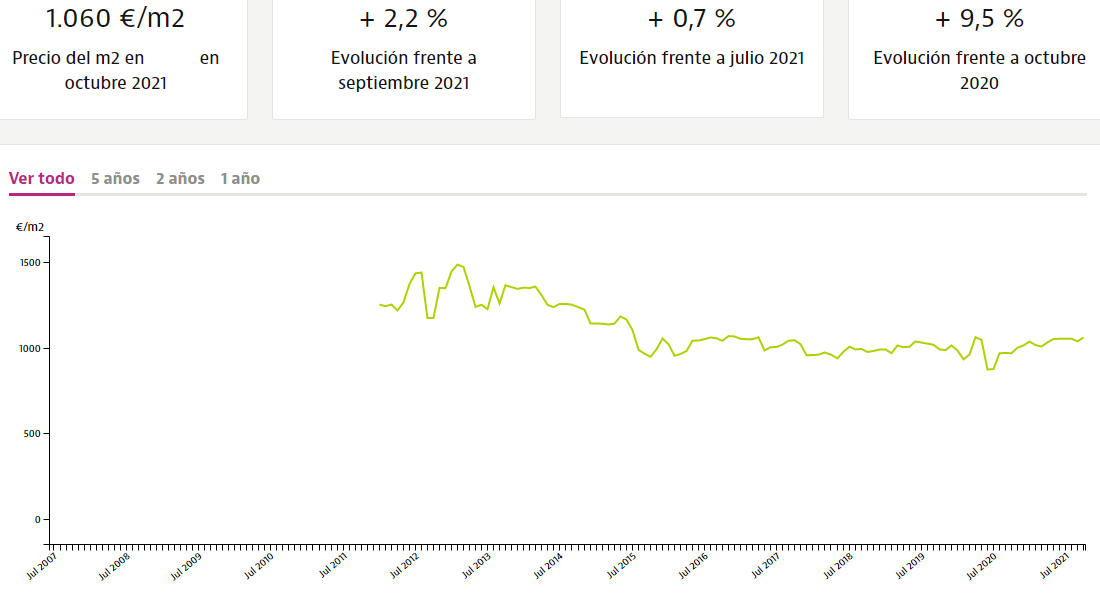

Then I last analysed the property market statistics. There are several websites showing property data, but I noticed some info is not consistent among them. This variability made me think that I should take the info with a pinch of salt. As far as I am aware, Idealista.com is one of the most advanced and reliable sites in Spain and Portugal. I personally like this site as it shows you the €/m2 price of the area you want.

That’s an overview of the price evolution of my flat location:

The first thing I notice is that the price trend over time is not taking the direction I’d like to see.

The €/m2 price in 2012 was as high as €1,439/ m2. That compared to today’s €1,060/ m2 gives a 26% total decline during a period of 9 years.

Ouch! That’s not a great place to start, is it?

I could stop researching right here and just go to the nearer real estate agency and ask them to sell my flat as soon as.

But, I am still curious to see a comparison of how much I could potentially make by renting, and by selling plus investing in stocks.

So, let’s continue.

I’ll use €1,060/ m2 as the starting point.

Taking that my flat is 80 m2 big: 80 m2 x €1060,= €84,800.

€84,800 should be the theoretical value of my flat, but, remember that I said I was not too sure about the data reliability that I found online? Because of that reason, I am going to apply a 10% reduction to that price, just to give it some “margin of safety”.

So, the final price I think I can sell my flat is €84,800 x 0.9 = €76,320

2. Estate agency’s fees

Although €76K is the price that I can aim for when selling, it’s still far from the actual net value I will get in my bank account.

My preferred method for finding a buyer is via an estate agency, and they are certainly not working for free as you can imagine.

Most agencies will charge you between 3%-5% of the final selling price. In my case that could range between €2,290, and €3,816. I emailed the four more well-known agencies in the area and asked them for a quote. The cheapest charges me a fixed fee of €3,000 with no dependence on the selling price. That’s the value I’ll take as a reference for my calculations.

So, €76,320 – €3,000 = €73,320

Let’s continue with the most exciting part…

3. Taxes

Me selling a property in Spain means I will need to pay a certain amount in taxes.

This is a complicated aspect. The calculations to determine the final amount depend on many factors, many of which are unknown to me.

However, taking a rough estimate should do for the practice of this exercise.

To make it easier, I’ll take the tax amount as €10K.

So, €73,320 – €10,000 = €63,320 (net selling price)

🙁

4. Expected Annual Returns After Selling

Now that I know the actual net value I would get after selling the flat, I can determine an estimation of how much I could gain if I invested this money elsewhere.

Back in June 2020, I took the firm decision of investing mostly in World Index Funds Accumulators. Some investors and analysts argue these days that the stock market returns for the next decade will be disappointing. However, no one can predict the future for certain, so, for the sake of simplicity, I am going to make two estimations, an optimistic one using the historic 8% annual return, and a neutral one using a 5% as annual return.

- Optimistic scenario: €63,320 x 8% / 100 = €5,066

- Neutral scenario: €63,320 x 5% / 100 = €3,166

The good thing about being in accumulators is that returns are automatically reinvested. This has the advantage of not having to pay income tax of any kind during the accumulation phase, even in Spain.

5. Determining a Renting Price

Having now found out a hypothetical yearly return to my selling case, it’s now time to calculate how much I could make If I would rent instead.

The first thing I need to do is to determine a gross renting price.

For that, I can follow the same steps I did when determining a sale price.

I talked to neighbours, checked online, and came to the conclusion that I could rent it approximately for €450/month.

So, €450/month x 12 months = €5,400 a year of gross passive income.

6. Expenses and deductibles

Owning a house has some expenses, so that €5.4K is not close to the net yearly return I can gain from renting.

These are all the yearly fixed expenses I must face as an owner of the property:

- Home insurance: €147.1/y

- Service charges: €720/y

- Maintenance costs: 1% of €84,800 = €848/y

- IBI (council tax): €192.6 /y

- Amortization (approx.): €100

- Total fixed annual expenses: €2,007.7

If I manage to rent the flat, then I will avoid the annual service charge expense of €720 as this is normally covered by the tenant.

My total annual expenses for being an owner in the scenario of renting would be €2,007.7 – €720 = €1,288.

It’s worth noting that these expenses are tax-deductible, which means it will help me reduce the tax bill on rental income.

7. Taxes on Renting

Taxes on renting are slightly a bit more complex, but I managed to get a much clearer view on how to calculate them than in the selling scenario.

My annual rental income is €5,400.

Deducting my €1,288 of annual expenses gives me €4,112 of pre-tax income.

On that amount, I need to apply a 60% reduction before determining the final tax bill, so €4,112 x 0.6 = €2,467.2

€2,467.2 is my taxable amount.

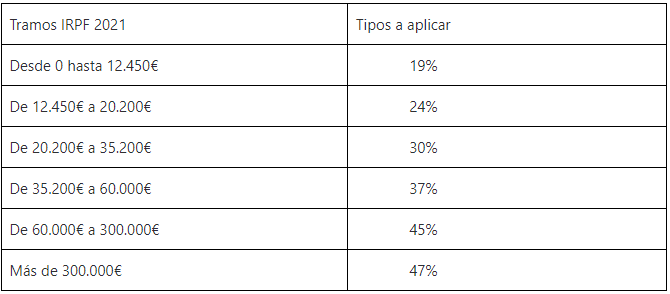

These will be taxed following the current tax income rates (IRPF) as a Spanish resident.

These are the ones for 2021:

My amount falls within the 19% range, so the tax bill will be €2,467.2 x 0.19 = €468.77

As I understood it, these rates apply if you are a Spanish or EU resident. The non-EU resident tax rate is 24%. That means if I were to move back to the UK and become a resident there, my tax bill would be higher, 2,467.2 x 0.24 = €592.13.

In my calculation, I’ll use the EU rate and therefore the amount of €468.77.

If all this sounds confusing, are interested in learning more, and you understand Spanish, check this out.

8. Expected Annual Returns If Renting

Now that I have all the numbers I need, it’s about time I get to the interesting bit — the annual returns.

Once I have paid those lovely taxes, I will be left with a net amount of €3,643 in my bank account. This amount translates into a net yield of 5.75% (based on the net selling price of €63,320).

A net yield of 5.75% looks good at first. The rental prices in the area are quite high compared to the property value. However, the declining trend on the property price puts me off. I doubt the price could go much lower with the current high inflation environment, but expecting any interesting growth would be a mistake. The business activity in the area is declining, and I don’t see this changing anytime soon as we enter a digital/high-skilled era.

9. Compounding comparison

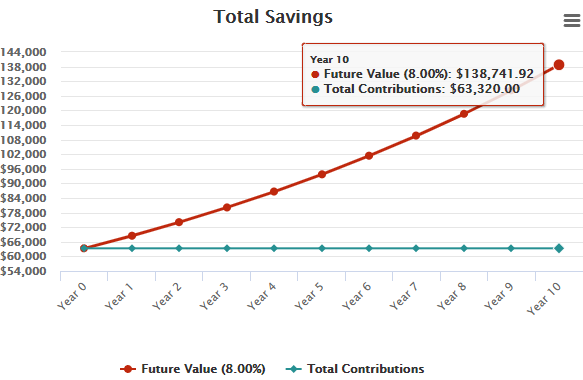

The last thing I want to do is to project how much I will have in 10 years’ time. I will use a compound calculator, and take the following data:

Selling:

- Initial investment: €63,320

- Monthly contribution: €0

- Years: 10

- Interest rate: 8% (optimistic) 5% (neutral)

- Compound frequency: Semi-annually

– Value after 10 years (optimistic): €138,472

– Value after 10 years (neutral): €103,757

Renting:

- Initial investment: €63,320

- Monthly contribution: €303.6 (100% occupancy), €243 (80% occupancy rate)

- Years: 10

- Interest rate: 2% (optimistic), 0.5% (neutral)

- Compound frequency: Monthly

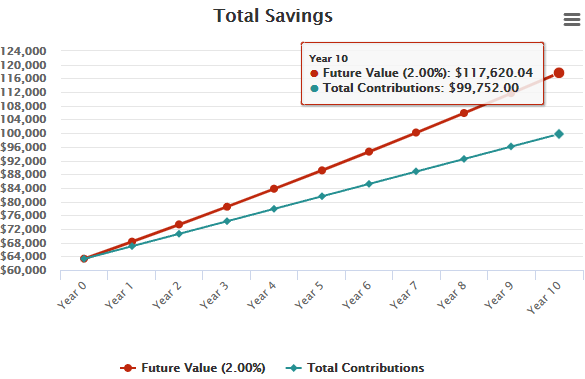

– Value after 10 years (optimistic): €117,617

– Value after 10 years (neutral): €96,460

Putting the basics together:

| (Optimistic scenario) | Return In 1 year | Projected Value In 10Y |

| Selling | €5,066 | €138,472 |

| Renting | €3,643 | €117,620 |

Final Words

As an overall and final comment, I can see that I’ve got a better chance at ending in a better financial position if I sell and invest in index funds accumulators than If I rent.

Obviously, this is only a basic analysis. There are many other possibilities that could occur, but in most cases, I still think I would do better if I sell. If the stock market goes down, it would mean the economy is not doing well as a whole, and therefore the chances I can increase my rent or enjoy an asset appreciation would be minuscule in a negative stock market scenario.

Another thing to consider is time. Renting means I need to hustle to sort out taxes every year, I need to fix toilets, I need to worry if a tenant doesn’t pay. If I wouldn’t want to worry about any of this, I’d need to hire an agency to deal with it, which means more fees and lower net returns.

Selling and investing it in index funds also gives me greater freedom of choice. I can move wherever I want without having to worry about anything of the above. Renting would need to be way more profitable than selling for me to give up on freedom.

And to top it up, we got the liquidity bit. Selling and investing in index funds allows me to have quick access to my capital whenever I want to and wherever I go, which is another important aspect for me if you ask.

Nonetheless, I would like to hear your thoughts on this. Do you think I am making the right decision? Or perhaps, I am missing something that I should be taking into account?

If you found this post insightful and helpful, would love to know about it, and yeah, why not share it with others? 🙂

19 Comments

Comments are closed.

ABOUT ME

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

Hi there! It's Tony here and I am hoping to post my journey towards one million euros.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

NET WORTH GOAL

Hey Tony,

Great article, I’ve just purchased a rental property myself and I hope the workload won’t kill me!

One other scenario you didn’t use was to take out a mortgage for the property and invest this in an indes Fund whilst also renting the property out.

This way you would get a far better return and really leverage the value of the property. Also, the interest costs would be tax deductible or?

Best

Steve

Thanks Steve,

You are right, I didn’t consider that option. Maybe it’s worth having a check on what rates I could get and run some more numbers before taking any final decision.

I understand why owning real estate in an area where the prices have been steadily declining for a long time doesn’t appeal to you.

From your analysis I think selling it makes sense.

On the other hand: your calculations of net return on renting the property should be based off YOUR purchase price. If I remember correctly, you inherited it, right? So it’s your purchase price is 0. Making any passive income 100% ROI 😛

Like Steve said, you could take out a mortgage? Would that make sense? This is the main reason why you should own real estate – to leverage its value to purchase more assets 🙂

But piece of mind is also worth a lot, so if you have decided to sell it then get it done ASAP 🙂

I’ll need to check out the mortgage option. TBH, I didn’t consider it as an option, but it makes sense to run some number at least to learn more about the process and how much leveraging could benefit me vs risks.

Hi Tony,

where on Idealista.com can you do this analysis? I cannot find it. Would you mind point me to it?

Thanks, Manfred

Sure, check this out, Manfred:

https://www.idealista.com/sala-de-prensa/informes-precio-vivienda/venta/cataluna/barcelona-provincia/barcelona/

Once there, it gives you the option to choose the location you want.

It is a great analysis. The renting raises with the IPC 2,5% for the next years and you have paid taxes already so it is 100% your money.

Thanks, Pedro.

Most renters struggle to pay €450 a month in my area, as it is not having an economically strong days. I am not too sure if I’d be able to raise the rent much, though I am entitled to raise the as IPC rates annually, as you say, I would consider it unethical, unless they would earn some type of government benefit, of course!

Thanks for your comment 🙂

Interesting numbers! I did a similar exercise not so long ago to decide whether buying to rent here in the Emerald Island would be a good idea. Yield was even lower than the one you calculated so it was a hard no-way. Historically real state has always been a very safe bet when it comes to investing, however that usually comes with low yields and initially very little passive income since you have to keep you have to manage the property. I barely do my chores at my place, wouldn’t have time to do them in a different place, so I would probably pay someone to do it which makes the yields even lower :(.

Perhaps a good play would be to have a property in Ireland/UK (or any other expensive housing market in EU) and live in a sunny southern Portugal. Just saying 😛

Running some number always helps, doesn’t it? I would enjoy managing the property myself, so as you say, paying those fees to an agency makes it even less profitable.

I rather invest my time learning about stocks, crypto, reading interesting material, or learning some new skills than fixing toilets.

Take care man!

Real estate can be difficult as an investment comported to stocks. They maintenance costs are always unexpected.

Yeah, tell me about it. We recently had to spend over €3K to fix the roof after we had a few days of fierce winds.

Great post Tony.

I too hope to sell my own BTL (when I am able to). Before all the issues with the cladding, my net yield had been around the 7% mark but last year, I lost money as the rent received didn’t cover all my charges.

Rental income is not passive and I think I would like an easy life!

Thank you weenie 🙂

The fire issues with the cladding hit hard in the UK. I got some property shares on Property Partner which value has dropped -40% because of the cladding issues.

No one could have anticipated the Grenfell Tower fire and the consequences it would bring. Imagine you decide to move one year to Hong Kong after RE and have to deal with cladding/paperwork issues when there! 🙁

Good luck with selling your BTL, and hope it goes easy for you.

[…] stay, my global impression is that Portugal is a well-rounded place to FIRE. Since I have plans of selling my flat and removing roots from Spain in the short term, relocating to Portugal remains on the table as an […]

[…] we are “settled” back in Spain in that flat I am supposed to be selling at some point. We’ll stay here until our next adventure begins, which given the current virus […]

[…] my flat for selling through an estate agency. Agent thinks I may get a chance to sell it for €100K. That’s more […]

[…] despite being another bad quarter for investments. The reason for this is that I found a buyer for my flat who was willing to pay more (€90K) than I originally accounted for in my books (€72K), so this […]

[…] write a blog post summarizing the numbers, so then I can compare it with those I considered in this blog post, but I am finding it hard to get the time for it. I am glad I found a spot to write this […]